China continues coal-reliant investments in the steel sector, threatening to derail the country’s climate commitments, create a slew of exorbitant stranded assets, produce more steel than the market demands, and ultimately make the sector financially vulnerable, a new report by the Centre for Research on Energy and Clean Air (CREA) finds.

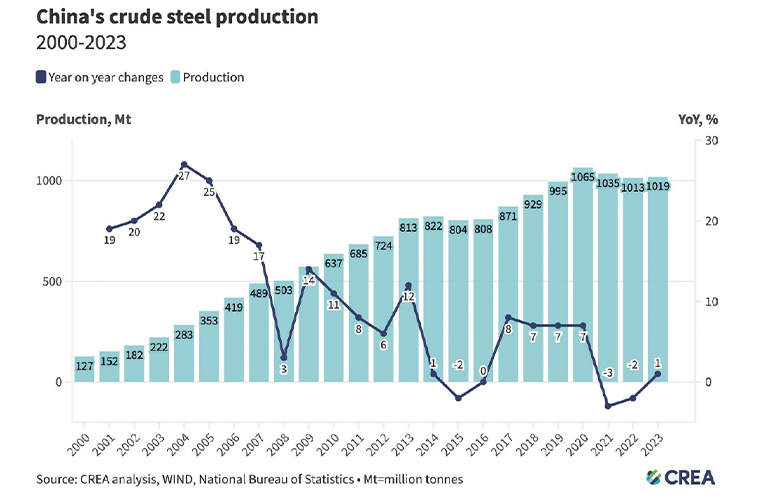

China is the worldʼs biggest steel producer and contributes to more than half of the global steel output.

Accounting for about 17 percent of the country’s total carbon emissions, the steel sector is the second largest contributor to carbon emissions – China’s power sector is the largest carbon emitter.

However, when emissions from the steel sector’s power consumption are included, the sector tops the list as the biggest carbon emitter in China.

Assets worth US$118 billion at risk

A Finland-headed independent research organization, the Centre for Research on Energy and Clean Air (CREA) is focused on revealing the trends, causes, and health impacts, as well as solutions to air pollution.

CREA’s latest report has revealed that Chinese steel plants approved after 2020 risk becoming stranded assets worth US$118 billion.

If China is to meet its climate targets, it will require the retirement of these carbon-intensive facilities before the end of its operational lifetime.

These coal-based plants that contribute to China’s steel sector make it among the highest carbon-intensive producers in the world.

Unfortunately, China has scrapped the ambitious push for its steel industry to peak carbon emissions by 2025, pushing the deadline back five years in its final guidelines. The steel sector will now have until 2030 to peak its emissions, which is in line with Chinaʼs broader national target, said Xinyi Shen, Researcher at CREA and author of the report.

High-carbon low demand

On average, China generates over two tonnes of carbon dioxide (CO2) for every tonne of steel (2tCO2/t) it produces. By comparison, the United States (US) has a carbon emission intensity of under one tCO2/t.

The global average is 1.91 tCO2/t. This is mainly attributed to the high carbon intensity and global share of Chinese steel.

Several models also show that China’s steel demand will decline significantly as industrialization and urbanization peak.

One model expects the country’s crude steel production to decline 58 percent by 2050 compared with 2020.

The sector is already accelerating towards exorbitant stranded assets. In 2023, the sector’s annual fixed asset investments (FIA) were 14 times its total profit.

Policy recommendations

Despite being the second largest source of carbon dioxide, investments in new production capacity are not aligned with China’s ambitious ‘dual carbon goals’ to reach CO2 emissions peak before 2030 and achieve carbon neutrality before 2060.

There is still a lack of an official timeline for Chinaʼs steel sector to become carbon neutral. To meet the national broader 2060 carbon neutrality goal in combination with the demand decline will require early retirement of carbon-intensive facilities. Therefore, the new blast furnace-basic oxygen furnace (BF–BOF) projects approved in 2021–2023 alone will face the risk of ending up as stranded assets worth CNY 850 billion (US$118 billion). If BF–BOF projects approved in 2017–2020 are included, there will be CNY 1,956 billion (US$270 billion) more risks in stranded assets, Xinyi Shen said.

To ensure a quick transition towards cleaner steel production, CREA proposes the following policy recommendations:

- The steel sector should be included in China’s emissions trading system (ETS) within the 14th five-year period. The ETS should shift from an intensity-based allocation to an absolute cap.

- To peak CO2 emissions from the iron and steel sector before 2025, new investments in blast furnace capacity should be limited and the adoption of electric arc furnaces and hydrogen-based steelmaking technology sped up.